The Risk and Impact of Living Longer

As appeared in Financial Advisor Magazine

There’s no denying that longevity is increasing in the U.S. and throughout much of the world. Recent legislation like The SECURE Act, passed on May 23 by the House of Representatitves, is beginning to recognize this trend and the potentially far-reaching implications on society. One much-publicized provision of this bill is a proposed delay in the required-minimum-distribution (RMD) age from 70 ½ to 72. The bill also proposes a change that would allow IRA contributions for all workers with earned income, regardless of their age, along with rules requiring employers to allow long-term, part-time workers to participate in company 401k plans. These changes are driven, in part, by expectations that greater longevity will result in more workers choosing and needing to remain employed beyond age 70.

A potentially negative consequence of the bill (as currently proposed) is limiting the “stretch IRA” provisions to 10 years if an IRA is inherited from a parent or spouse. These changes are likely to impact clients’ financial plans and strategies for transferring family wealth. The bill’s recognition of greater longevity also begs the question, “How can financial advice better incorporate longevity risk planning in ways that are meaningful to clients?”

As the Senate debates The SECURE Act, we weigh in on some of the potential financial planning implications of longer lives and suggest ways to quantify and communicate potential risk to clients. Our goal is to inspire advisors to ask what actions to consider in response to the greater longevity we’re witnessing among clients and in society as a whole.

Bearing vs. Sharing Longevity Risk

One of the more obvious challenges we face in retirement planning is that individuals are increasingly required to bear longevity risk. Prior generations enjoyed having longevity risk largely covered (or at least shared) with employers via lifetime income benefits from defined-benefit plans. Today’s workers usually are not so fortunate. According to the U.S. Bureau of Labor Statistics, as of March 2018, on average, only 3% of full-time private-industry workers had access to a defined-benefit plan. In comparison, 58% of these same workers only had access to a defined-contribution plan. These figures show just how widespread the longevity risk shift is and the importance of our role in helping clients manage that risk to create sustainable retirement income plans.

While the decline in defined-benefit plans has been accompanied by greater access to defined-contribution plans, like 401Ks, there is little evidence that these new plans are adequate replacements. First, maximizing contributions can be challenging, especially given that workers face increased basic living costs, including higher housing and health-insurance expenditures. A study by the MIT Age Lab showed 35% of student loan balances were held by individuals over age 40. Higher living costs and debt levels challenge employees’ ability to contribute up to defined-contribution plan legal limits. For those who do achieve maximum contribution levels, many are constrained in their ability to accumulate the additional, non-plan savings required to adequately cover the longevity risk they’re now forced to bear.

Workers also shoulder greater market risk to their retirement plan values, both while they’re working and throughout a potentially much longer period of retirement. Consider a retirement that lasts only 20 years (say, age 65 to 85). It’s reasonable to expect investors might face two or three bear markets during that retirement period. That means the risk of losses or of getting shaken out of the markets is very real, perhaps even more so if they don’t have the benefit of expert investment management to manage through down cycles. This risk is exacerbated by the very real prospects for lower capital market assumptions over the next several years.

Recognizing “Grey Divorce” and the Possibility of New Spouses

Another trend that may be the result of living longer is the increase in the number of “grey divorces.” While we may be living longer, some marriages aren’t lasting over extended life spans. The trend of more divorces of individuals over age 50 reflects reduced stigma around divorce, greater health, and the increasing economic independence available to women.

Increasingly, even long marriages are are risk. One interesting finding in a 2017 Pew Research Center report is that “Among all adults 50 and older who divorced in the past year, about a third (34%) had been in their prior marriage for at least 30 years, including about one-in-ten (12%) who had been married for 40 years or more. Research indicates that many later-life divorcees have grown unsatisfied with their marriages over the years and are seeking opportunities to pursue their own interests and independence for the remaining years of their lives.”

It seems reasonable that as people live longer, we’re likely to see even more couples deciding to split much later in life, potentially during their retirement years. Consider a couple who carefully saves for retirement, transitions to a long-imagined lifestyle and then decides to part ways. If years of financial decisions such as retirement timing, asset titling, and spending budgets were established assuming a lifelong, happy marriage, a grey divorce can upend even the most prudent retirement planning decisions.

Late-in-life divorces also bring the possibility of new spouses with them. Obvious challenges are asset protection and creating estate plans that balance the new spouse’s needs with those of existing heirs. If the new spouse is younger, planning for potentially more cash flow and portfolio longevity requires the couple to have a larger asset base. This challenge is compounded when assets or income sources have been partially dissipated in a divorce. At a minimum, advisors can provide detailed analyses of potential retirement spending early in the new relationship. That way both parties are clear about the financial, lifestyle and potential estate plan implications of taking on a new spouse.

Analyzing Potential Delays or Dissipation of Inheritances

Clients can also be impacted by the greater longevity of their parents and the effect that has on the transition of family wealth. Inheritances may be delayed, or assets may be dissipated if aging parents incur significant healthcare care costs. Parents may simply live longer, which may delay heirs’ access to the assets. Owners of lucrative family businesses may elect to stay in the business longer, deferring transfer of income production or the ultimate wealth transfer to heirs.

For Boomers living their lives expecting an inheritance to cover their own longevity risk, a delay or loss of inheritance could be a rude awakening. While difficult to quantify, the prospect of living a longer life may reduce the likelihood that parents will make significant gifts to their children while still alive. Imagine the potential impact on their retirement lifestyle if the reality of lower lifetime gifts, or reduced or no inheritance, comes later in a client’s lifecycle when it may be too late to replace the lost inflow of those expected assets.

Potential Responses

One way to manage longevity risk is to utilize insurance products that attempt to share risk with an insurance company. This topic warrants an article all its own, so suffice it to say that products like hybrid long-term care policies are just one example of a range of products aimed at offloading some longevity risk. Insurance products may also be helpful tools to use in grey divorces to secure a newly single woman’s life or in pre-nuptial arrangements to provide assets for children or a new spouse.

If clients are focused on paying unexpectedly high costs for care at the end of life, margin or other debt lines can be another tool. Consider, for example, an only child who needs cash flow to support his father’s care needs. His father’s estate plan could be revised to incorporate a payback provision, and the family could thereby benefit from preserving the asset base. Taxes can also be saved by foregoing large capital gains, while additional tax savings could come from utilizing a stepped-up basis upon the father’s death.

Beyond these tactical responses, we suggest using technology to help quantify and shed light on longevity risk in the context of each client’s specific circumstances. The goal is to provide the advisor and clients opportunities to ponder how longevity risks could derail an otherwise solid plan. The process is also a way to start a conversation with clients around reviewing insurances, working longer, or adjusting spending budgets as ways to secure a plan in the face of longevity risks.

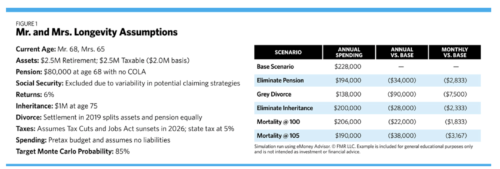

In the following example, we illustrate potential impacts that longevity-related risks could have on annual and monthly retirement spending budgets. As you’d expect, the impact of a grey divorce creates the greatest reduction in potential annual spending. Consider the effect it could have if a client also takes on a second spouse who has little or no assets. The loss of a $1 million inheritance would reduce the “safe” monthly spending budget by an estimated $2,333 each and every month of a 30-year retirement. It’s also significant to note that increasing longevity to age 105 would reduce guideline annual spending by $38,000 per year from $228,000 to $190,000. The goal here is not to focus on the precise numbers but rather to display, in directional terms, how much clients may want to reduce current expenditures in order to provide a longevity safety net. To the extent more than one of these events occurs, the financial impacts compound. Running plans for younger clients may introduce even greater variability between model and actual outcomes due to a greater likelihood of any given event over time plus less certainty about exactly how much longevity could improve for younger generations.

Conclusion

As advisors, it’s our responsibility to spot trends in the lives of our clients and to develop and provide tools and solutions for managing the numerous risks life can deliver, including longevity risk. As an industry, we must continue to work together to identify trends and provide solid, practical solutions for clients and families who depend on our foresight and ability to balance protecting them from longevity risk with helping them build the wealth required to enjoy the longer lives they (and their parents) are likely to live.