Is this rate cycle different?

Federal Reserve Chair Janet Yellen signaled last week that monetary policy is on the path to normalization and that the long period of extremely accommodative short term interest rates is over. The Fed must act with unusual care, however, as this interest rate cycle is unlike any previous one.

What makes this cycle unique?

- The starting point: The Fed funds rate bottomed at nearly zero before the December 2015 0.25% bump, and the 10-year Treasury bond sank to 1.36% last July.

- The length of time: The period of near-zero rates began December 2008 and lasted seven full years.

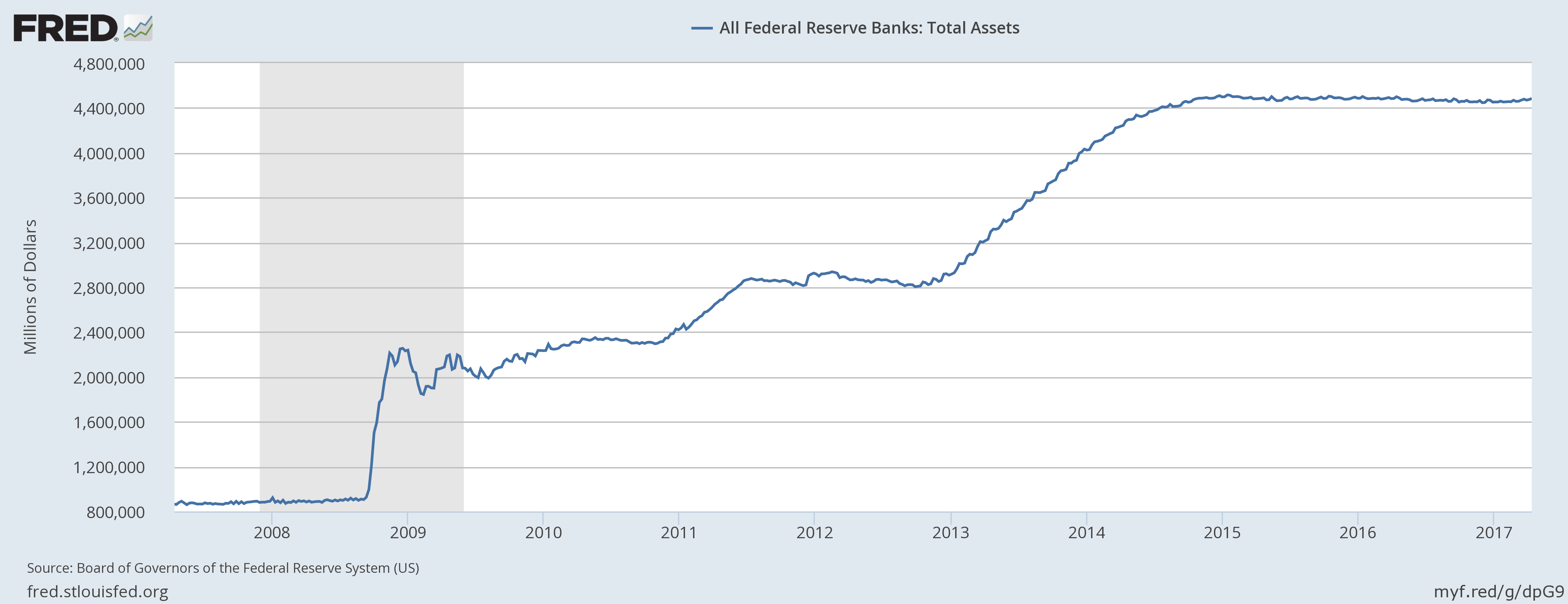

- Quantitative easing: Not only did the Fed slash short term rates starting in 2008, but it also bought government and mortgage-backed bonds in the open market at longer maturities, swelling its balance sheet from $862 billion a decade ago to $4.5 trillion today.

- The advanced stage of the cycle: The Fed has never before waited this long into a business cycle before embarking on a series of rate increases. Additionally, the Trump administration’s policy goals include tax reform and infrastructure spending that would provide a spending boost that has generally only occurred when emerging from recession.

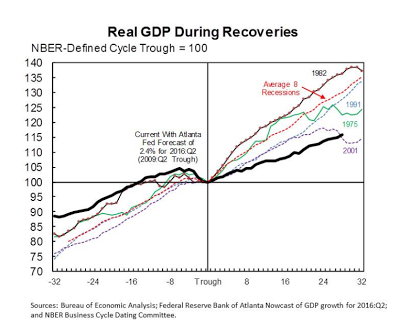

- The shallow recovery: Despite the unprecedented stimulus, GDP growth has been subdued, lagging previous recoveries, and the slow growth has been a global phenomenon.

What issues do these points present for the Fed and financial markets?

- When rates are so low, bond prices are more sensitive to upward movement (prices move inversely to yields). For example, the 10-year Treasury posted a total return of (8.4%) from July through December 2016. Sudden losses could prompt selling that spills into other financial assets and undermines confidence in the economy.

- Financial markets have not had to contend with a succession of rate increases since the 2004-2006 cycle. Many participants have experienced only fleeting losses on fixed income holdings, and bond markets could have trouble digesting a surge of selling from weaker hands, impeding capital formation.

- At some point, possibly later this year, the Fed will stop reinvesting the proceeds of maturing assets and allow its balance sheet to shrink, which will effectively tighten monetary conditions. The problem for the Fed is that no one knows what the impact will be on the markets or the real economy. Over a third of the assets the Fed holds are mortgage-backed securities; if the Fed lets those run off, could mortgage rates rise in the absence of such a large buyer?

- In addition to managing the rundown of its balance sheet, the Fed may also have to contend with a jolt of fiscal stimulus, something highly unusual this far into an economic cycle. If inflation surges above the Fed’s 2% target, it may be forced to raise interest rates quickly, which could in turn precipitate a recession.

- On the other hand, real GDP growth has yet to top 3% during any single year of what is now approaching a nine-year recovery. That makes it more likely that the Fed will err on the side of keeping rates lower for longer, but with the economy reaching full employment and wage growth beginning to gain traction, inflation becomes a greater risk.

In sum, the Fed is walking a twisting policy path, one only dimly illuminated by macroeconomic and political conditions and replete with potential missteps. Bonds currently appear to be the asset class most at risk in the near term, and we have generally shortened duration and expanded our non-traditional fixed income portfolio in anticipation. We continue to look for signs that the Fed is becoming overly aggressive as a possible signal to become more defensive with our equity positioning.